Retirement Planning 2026: How to Build ₹5 Crore Retirement Corpus by 2040 with Just ₹10,000 Monthly SIP

Retirement planning 2026

⚠️ Important Disclaimer Mutual fund investments are subject to market risks. Read all scheme-related documents carefully. Past performance is not indicative of future results. This article is for educational purposes only. Consult a SEBI-registered financial advisor before making any investment decisions.

🚀 Introduction: Can ₹10,000 Monthly SIP Build a ₹5 Crore Retirement Corpus by 2040?

Imagine starting with just ₹10,000 per month in April 2026… staying consistent… increasing your SIP every year… and building a retirement corpus of ₹4–5 crore+ by 2040.

Sounds ambitious? It is. But with the power of compounding, step-up SIP, and smart equity allocation, it is realistically achievable for disciplined investors.

In April 2026, the Nifty 50 is trading in the 22,800–23,000 range amid volatility. Yet, this is precisely when long-term retirement planning through SIPs shines — thanks to rupee cost averaging.

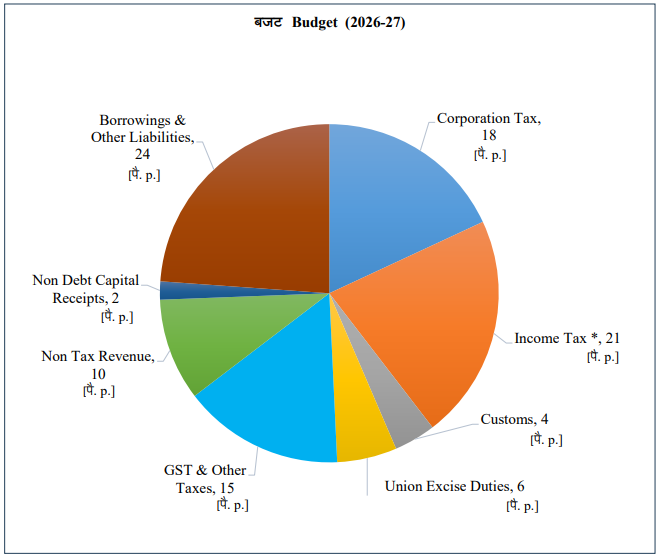

The Union Budget 2026 has further strengthened the case for equity investing with a record ₹12.2 lakh crore public capital expenditure (capex) push — a 9% increase from the previous year. This massive infra, manufacturing, and banking focus creates long-term tailwinds for equity and hybrid mutual funds.

Most people delay retirement planning because:

- “I’ll start when I earn more”

- “₹10,000 is too little”

- “Markets look high right now”

This guide shows you exactly how starting today with ₹10,000 SIP + 10% annual step-up can help you reach your ₹5 crore goal by 2040.

What You’ll Learn:

- Realistic growth projections with step-up SIP

- Phased asset allocation strategy for 2026–2040

- Best mutual fund categories & examples

- Common mistakes to avoid

- Pro tips & FAQs

📊 Why Retirement Planning Matters More in 2026 (Retirement Planning 2026)

- Rising Inflation — ₹1 crore today may feel like ₹40–50 lakh in purchasing power by 2040 (at 6% inflation).

- Longer Life Expectancy — You may need income for 25–30 years after retirement.

- Decline in Traditional Pensions — Most private-sector jobs offer limited or no pension support.

Bottom line: You must build your own retirement corpus through disciplined SIP investing.

💡 The Power of SIP + Step-Up for Retirement

SIP removes market timing stress. Adding 10% annual step-up dramatically multiplies your corpus through higher contributions + compounding.

Illustrative Projections (₹10,000 Starting SIP with 10% Annual Step-Up) (Assuming investments from 2026 to 2040 — ~14–15 years)

| Scenario | Average Annual Return | Approx. Corpus by 2040 | Total Amount Invested (Approx.) |

|---|---|---|---|

| Conservative | 10–12% | ₹1.8 – 2.5 Crore | ₹35–40 Lakh |

| Moderate (Recommended) | 12–14% | ₹2.8 – 3.8 Crore | ₹35–40 Lakh |

| Aggressive | 14–16% | ₹3.8 – 5+ Crore | ₹35–40 Lakh |

Notes: Projections are illustrative. Actual returns depend on market conditions. Use online SIP calculators

🎯 Step-by-Step Strategy to Build ₹5 Crore Corpus

Step 1: Define Your Goal Clearly

- Desired retirement age?

- Monthly expenses today (e.g., ₹50,000) → Inflation-adjusted need in 2040: ~₹1.4–1.6 lakh.

- Target corpus: ₹4–5 crore (to generate safe withdrawal of 4–5% annually).

Step 2: Set Realistic Return Expectations Aim for 12–15% long-term average from a well-diversified equity-heavy portfolio (achievable historically with flexi-cap and mid-cap funds, though not guaranteed).

Step 3: Phased Asset Allocation (2026–2040)

- Early Phase (2026–2032): 80% Equity + 20% Hybrid — Maximize growth.

- Middle Phase (2032–2037): 65–70% Equity + 30% Hybrid/Debt — Balance growth & risk.

- Pre-Retirement Phase (2037–2040): 50% Equity + 50% Debt/Hybrid — Focus on capital protection.

Step 4: Implement Step-Up SIP Start at ₹10,000/month and increase by 10% every year. This single habit can nearly double your final corpus.

💼 Best Mutual Fund Strategy for Retirement in 2026

Focus on Direct Plans for lower expense ratios.

Early Growth Phase Recommendations (High Equity Tilt):

- Flexi Cap: Parag Parikh Flexi Cap Fund, HDFC Flexi Cap Fund (global + domestic diversification)

- Large & Mid Cap / Mid Cap: HDFC Midcap Opportunities Fund, Nippon India Growth Fund

- Hybrid: HDFC Balanced Advantage Fund or ICICI Prudential Equity & Debt Fund

Why These in 2026? The Budget’s ₹12.2 lakh crore capex push benefits infrastructure, manufacturing, and banking sectors — areas where mid-cap and flexi-cap funds have strong exposure.

Rebalance annually and shift allocation toward debt as you near retirement.

🛠️ How to Execute This Plan

- Assess your risk profile and goal.

- Open an account click here

- Choose Direct Plans and set up monthly SIP + step-up feature (available on most platforms).

- Review portfolio once a year.

- Stay invested during market corrections — this is where SIP shines.

📈 Real-Life Case Study (Nagpur Salaried Professional)

- Age in 2026: 32 years

- Starting SIP: ₹10,000/month in moderate portfolio

- Step-up: 10% annually

- Strategy: Equity-heavy early on + annual rebalancing

- Stayed disciplined through market volatility

Result by 2040 (age ~46–47): Total invested: ~₹35–40 lakh Corpus: ₹4–5 crore (at 13–14% average return)

This is the real power of starting early + compounding.

📊 SIP vs FD vs Gold for Retirement (Long-Term View)

| Investment | Expected Long-Term Return | Risk Level | Suitability for Retirement |

|---|---|---|---|

| Equity SIP | 12–15% | Medium-High | Best for growth |

| Fixed Deposits | 6–7% | Low | Poor (inflation erosion) |

| Gold | 8–10% | Medium | Hedge, not primary |

💰 Tax Rules for Retirement Corpus (2026)

- Equity-oriented funds (≥65% equity): LTCG > ₹1.25 lakh taxed at 12.5%; STCG at 20%.

- Hybrid funds follow equity or debt taxation based on asset allocation.

- Hold investments long-term to optimize tax.

Tax rules are subject to change. Consult a tax advisor.

⚠️ Common Mistakes to Avoid

- Starting late or not stepping up SIP

- Panic selling during market crashes

- Ignoring expense ratios (always choose Direct plans)

- Over-diversification (limit to 6–8 funds)

- Chasing last year’s top performers

🌟 Pro Tips to Reach Your Goal Faster

- Start today — even if small.

- Increase SIP by 10–20% every year (or with salary hikes).

- Review and rebalance annually.

- Maintain an emergency fund separately (6–12 months expenses).

- Use retirement-specific or target-date funds if you prefer simplicity.

❓ FAQs

- Can ₹10,000 SIP really build ₹5 crore by 2040? Yes — with 10% annual step-up, long-term equity allocation, and 13–15% average returns, it can approach or exceed ₹4–5 crore.

- What is a realistic return expectation? 12–14% for a moderate equity-heavy portfolio over 14+ years.

- When should I reduce equity exposure? Start shifting 5–7 years before retirement for capital protection.

- Is SIP safe for retirement? Yes, for long horizons (10+ years). It reduces timing risk through rupee cost averaging.

- Best platform to start SIP? click here to open account

🏁 Conclusion: Your ₹5 Crore Retirement Journey Starts Today

Building a ₹5 crore retirement corpus by 2040 is not about luck or high income — it’s about starting early, stepping up regularly, and letting compounding work.

With the 2026 Budget’s strong capex focus creating growth opportunities, disciplined SIP investors are well-positioned.

Action Steps:

- Take 10 minutes today to calculate your own goal using a SIP calculator.

- Start or review your SIP portfolio.

- Increase contribution with your next salary hike.

Don’t wait for the “perfect” time. The best time was yesterday. The next best time is today.

📢 Call to Action 👉 What is your retirement target? Share your age and monthly SIP amount in the comments. 👉 Share this guide with friends and family who are planning for retirement. 👉 Consult a SEBI-registered financial advisor before investing.

⚠️ Final Disclaimer Mutual fund investments are subject to market risks. Read all scheme-related documents carefully. This is for educational purposes only. Past performance is not a guarantee of future results.

Why SIP is the Safest Investment Strategy

Best SIP Portfolios April 2026: Conservative, Moderate & Aggressive Strategies for Smart Investors

https://sarkariyojana24.co.in/

Open account for SIP in just 2 minutes click here

Share this content:

Post Comment