Your Financial Safety Net: How to Build an Emergency Fund That Actually Works

Life is unpredictable. A sudden medical expense, job loss, car repair, or family emergency can disrupt even the most carefully planned finances. What separates financial stress from financial stability in such moments is one powerful yet often neglected tool: an emergency fund.

Many people believe they have an emergency fund, but when a real crisis strikes, they realize it wasn’t enough, wasn’t accessible, or wasn’t protected from impulse spending. Building an emergency fund that actually works requires more than saving a little money occasionally—it requires strategy, discipline, and clarity.

This guide will walk you step by step through how to build an emergency fund that provides true financial security, using proven budgeting and saving methods that work in real life, not just on paper.

What Is an Emergency Fund?

An emergency fund is a dedicated pool of money set aside specifically for unexpected and essential expenses. It is not for planned purchases, vacations, or lifestyle upgrades.

True emergencies include:

- Medical emergencies

- Job loss or income disruption

- Urgent home or vehicle repairs

- Family emergencies

- Unexpected travel due to crisis

An emergency fund is not an investment. Its primary purpose is protection, not growth.

Why an Emergency Fund Is the Foundation of Financial Security

Before investing, before wealth creation, before long-term goals, an emergency fund comes first.

Without an Emergency Fund:

- You rely on credit cards or loans

- You may be forced to sell investments at a loss

- Financial stress increases dramatically

- One crisis can undo years of progress

With an Emergency Fund:

- You stay financially calm during crises

- You avoid high-interest debt

- Your long-term investments remain untouched

- You gain confidence and control

In simple terms, an emergency fund buys you time and peace of mind.

Common Myths About Emergency Funds

Many people delay building an emergency fund due to misconceptions.

“I don’t earn enough to save”

“My credit card is my emergency fund”

“I’ll start after I invest”

“Nothing bad will happen to me”

Reality check: Emergencies don’t wait for financial readiness. The right time to start is always now.

Step 1: Define What an Emergency Means for You

Not every unexpected expense is an emergency.

Ask Yourself:

- Is this expense unavoidable?

- Is it urgent?

- Does it impact basic living or income?

Clear definitions prevent misuse of your emergency fund.

Rule of thumb:

If the expense can wait or be planned, it is not an emergency.

Step 2: Decide the Right Emergency Fund Size

The biggest question people ask is:

“How much should I save in my emergency fund?”

The Standard Guideline

- 3–6 months of essential expenses

Essential expenses include:

- Rent or home loan EMI

- Food and groceries

- Utilities

- Insurance premiums

- Transportation

- Basic healthcare

Adjust Based on Your Situation

- Single income household → 6-9 months

- Freelancers or business owners → 9-12 months

- Dual income with stable jobs → 3-6 months

Your emergency fund size should reflect risk, not lifestyle.

Step 3: Calculate Your Monthly Essential Expenses

Before saving, you must know your number.

Create a Simple List:

- Housing

- Food

- Utilities

- Transportation

- Insurance

- Minimum loan obligations

Exclude:

- Dining out

- Subscriptions

- Shopping

- Entertainment

Multiply your essential monthly cost by your target months to get your emergency fund goal.

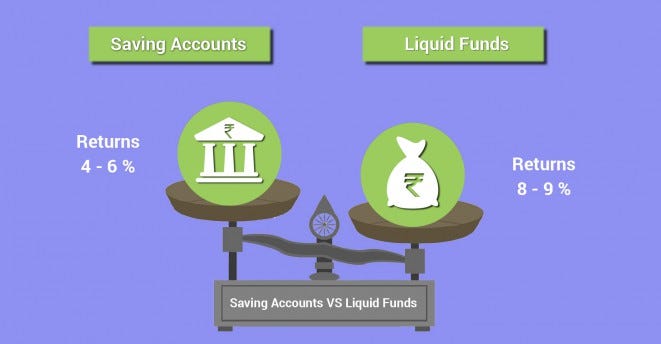

Step 4: Choose the Right Place to Keep Your Emergency Fund

Accessibility matters more than returns.

Best Options:

- High-interest savings account

- Liquid mutual funds

- Short-term fixed deposits (with instant withdrawal)

Avoid:

- Equity investments

- Long lock-in instruments

- Risky or volatile assets

Your emergency fund must be safe, liquid, and stress-free.

Step 5: Start Small but Start Immediately

Waiting to save a “big amount” often leads to never starting.

Smart Approach:

- Start with a mini-goal (₹10,000 / $500)

- Automate monthly transfers

- Increase contributions gradually

Even small amounts build momentum and confidence.

Step 6: Build Your Emergency Fund Using Budget Planning

Your emergency fund grows through intentional budgeting, not leftover money.

Proven Budget Planning Techniques:

1. Pay Yourself First

Treat emergency savings like a mandatory bill.

2. 50-30-20 Rule (Modified)

- 50% needs

- 30% wants

- 20% savings (emergency fund first)

3. Expense Tracking

Track spending for 30 days to identify leaks.

Every rupee or dollar saved intentionally strengthens your financial security.

Step 7: Increase Savings Without Increasing Stress

Saving should not feel like punishment.

Practical Emergency Fund Tips:

- Redirect bonuses or tax refunds

- Save side income fully

- Reduce one recurring expense

- Use salary increments wisely

Temporary lifestyle adjustments can create permanent financial stability.

Step 8: Protect Your Emergency Fund from Yourself

An emergency fund fails if it’s too easy to misuse.

Smart Protection Methods:

- Keep it in a separate account

- Rename the account “Emergency Only”

- Avoid linking it to daily spending apps

Psychological barriers are as important as financial ones.

Step 9: Know When to Use Your Emergency Fund

Using your emergency fund is not failure-it’s success if used correctly.

Valid Reasons to Use It:

- Medical emergencies

- Job loss

- Critical repairs

Invalid Reasons:

- Sales or discounts

- Lifestyle upgrades

- Planned expenses

After using it, rebuild it immediately.

Step 10: Rebuild After an Emergency

Emergencies will happen-that’s the point of the fund.

Rebuilding Strategy:

- Resume monthly contributions

- Temporarily reduce discretionary spending

- Use any windfalls to refill

Think of your emergency fund as a reusable safety net.

Emergency Fund vs Insurance: Know the Difference

Both are essential but serve different purposes.

Emergency Fund:

- Covers immediate expenses

- No approval or claim process

- Flexible usage

Insurance:

- Covers large, specific risks

- Requires documentation

- Takes time to process

Together, they create complete financial protection.

How Emergency Funds Support Long-Term Wealth Creation

A strong emergency fund allows you to:

- Invest confidently

- Take calculated risks

- Avoid panic selling

- Stay invested during market downturns

Ironically, emergency funds indirectly increase long-term returns.

Common Mistakes That Break Emergency Funds

Investing emergency money

Underestimating expenses

Not adjusting for inflation

Using it for non-emergencies

Never reviewing the fund

Avoiding these mistakes keeps your safety net strong.

How Often Should You Review Your Emergency Fund?

Review at least:

- Once a year

- After major life events

- After income changes

As expenses grow, your emergency fund must grow too.

Emergency Fund Checklist

✔ Clear definition of emergencies

✔ 3–6 months of essential expenses

✔ Separate, liquid account

✔ Automated contributions

✔ Protection from misuse

✔ Regular review

If these boxes are checked, your emergency fund truly works.

Financial Security Starts with Preparedness

Building an emergency fund is not glamorous. It doesn’t make headlines or promise quick returns. Yet, it is the most powerful act of financial self-care you can practice.

A working emergency fund:

- Reduces stress

- Protects investments

- Preserves dignity during crises

- Creates confidence

Financial freedom doesn’t start with investing—it starts with being prepared for the unexpected.

Start today. Start small. Stay consistent.

Your future self will thank you.

Top 10 SIP Mutual Funds with Highest Returns in 2026

Top Investment Ideas for 2026: Secure Returns with FDs, SIPs in Mutual Funds, Stocks, ETFs & More

Share this content:

Post Comment